Car owners today often customise their vehicles to improve comfort, performance and visual appeal. However, many are unaware that even minor changes can directly influence the IDV car insurance value and overall premium calculations. From alloy wheels to engine upgrades, modifications alter the vehicle’s original risk profile, which insurers consider while pricing policies.

Understanding how car modifications affect insurance premiums is essential to avoid claim issues, unexpected costs or coverage gaps later.

What are Car Modifications?

Car modifications refer to any change made to the vehicle after it leaves the manufacturer. These can be broadly classified into:

- Cosmetic modifications such as custom paint jobs, seat covers, infotainment systems or alloy wheels.

- Performance modifications, including engine tuning, turbochargers, suspension upgrades or exhaust changes.

- Structural or safety-related changes like altered chassis, body kits or external CNG/LPG kits.

How Car Modifications Impact Insurance Premiums

Under 4-wheeler insurance, premiums are calculated based on the vehicle’s risk exposure and Insured Declared Value (IDV). When modifications are made:

- IDV may increase if expensive accessories or performance upgrades are added.

- Repair costs rise as modified parts are often costlier and harder to replace.

- Risk perception changes, especially with engine or structural alterations.

As a result, insurers may increase the premiums to reflect the higher financial liability.

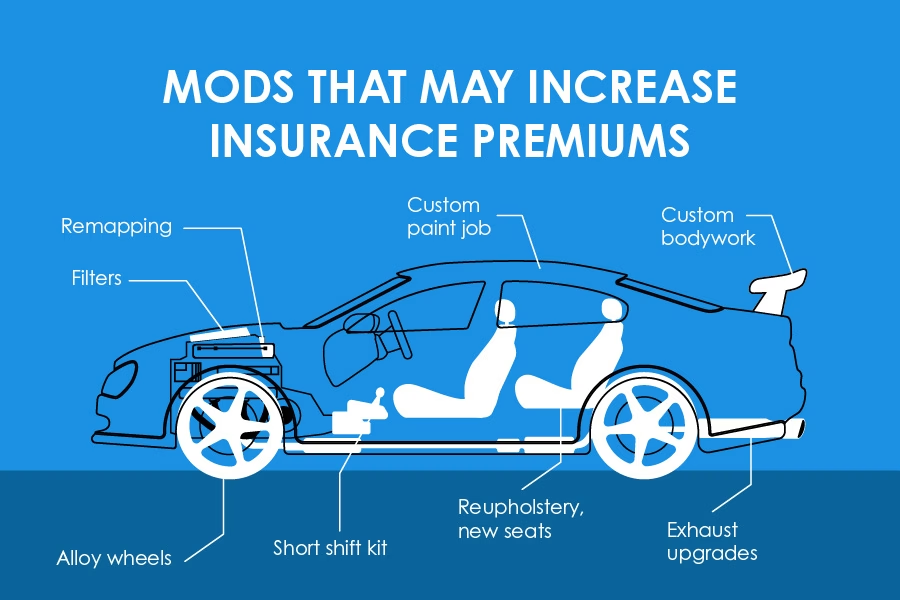

Types of Modifications That Increase Premium

Certain modifications almost always lead to higher premiums:

- Engine or performance upgrades that boost speed or power.

- Aftermarket electrical fittings, such as high-end audio systems or custom lighting.

- Exterior changes that alter the vehicle’s original structure.

Modifications That May Lead to Claim Rejections

Failing to disclose car modifications can create complications during claim settlement and may significantly reduce the payout. Insurers assess claims based on the vehicle details mentioned in the policy and any mismatch can raise red flags. Common risks include:

- Claim rejection if accessories or performance upgrades were not declared at the time of policy purchase or renewal.

- Partial claim approval when undisclosed modifications are found to have increased the extent of damage or repair cost.

- Policy cancellation or non-renewal in cases involving illegal, unsafe or RTO-unapproved alterations.

Additionally, if a modification contributes directly to an accident, such as an altered suspension or braking system, the insurer may question liability altogether. Since claim settlements depend heavily on declared specifications and approved endorsements, transparency is essential to ensure coverage works as intended when needed.

Importance of Declaring Modifications to the Insurer

Declaring modifications to the insurers during the 4-wheeler insurance purchase or renewal ensures:

- Accurate premium and IDV car insurance calculations.

- Proper coverage for added accessories.

- Smooth claim processing without disputes.

Most insurers allow endorsements to include modifications officially in the policy, ensuring coverage aligns with the vehicle’s current condition.

Avail Affordable Premiums with TATA AIG Car Insurance

Any modification made to a car, whether cosmetic or mechanical, changes how the vehicle is valued and how claims are assessed. Since premiums and IDV in car insurance are calculated on the basis of declared specifications, overlooking these changes can result in lower claim payouts or avoidable disputes. Informing the insurer about modifications promptly helps keep coverage accurate and aligned with the actual cost of repairs.

Insurers such as TATA AIG provide provisions to declare accessories and modifications through policy endorsements, allowing car owners to maintain valid 4-wheeler insurance coverage even after changes are made.

Leave a Comment

You must be logged in to post a comment.